All Categories

Featured

Table of Contents

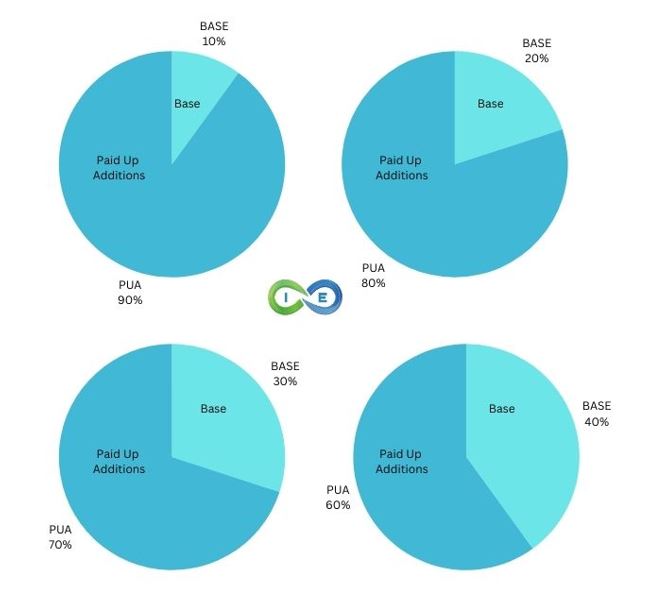

This provides the plan proprietor reward choices. Returns options in the context of life insurance coverage describe exactly how insurance holders can pick to make use of the rewards created by their entire life insurance coverage policies. Rewards are not guaranteed, nonetheless, Canada Life Which is the oldest life insurance company in Canada, has actually not missed out on a reward repayment given that they initially developed a whole life policy in the 1830's prior to Canada was even a country! Right here are the usual dividend options offered:: With this choice, the insurance policy holder utilizes the dividends to buy extra paid-up life insurance coverage.

This is just advised in case where the death benefit is extremely vital to the plan proprietor. The added expense of insurance coverage for the enhanced insurance coverage will decrease the money value, hence not perfect under unlimited financial where money worth dictates just how much one can borrow. It is essential to note that the availability of reward options may vary depending on the insurance provider and the details policy.

There are terrific advantages for limitless banking, there are some points that you ought to think about prior to getting right into limitless financial. There are additionally some disadvantages to infinite banking and it might not appropriate for someone who is trying to find cost effective term life insurance policy, or if a person is checking out purchasing life insurance policy only to secure their household in the occasion of their fatality.

It is essential to comprehend both the advantages and limitations of this economic strategy prior to making a decision if it's best for you. Intricacy: Infinite financial can be complex, and it is very important to comprehend the information of how a whole life insurance coverage plan jobs and just how plan lendings are structured. It is necessary to correctly set-up the life insurance policy policy to enhance infinite financial to its complete possibility.

How do I qualify for Wealth Management With Infinite Banking?

This can be particularly bothersome for individuals that rely upon the survivor benefit to attend to their liked ones (Financial leverage with Infinite Banking). On the whole, limitless banking can be a beneficial economic strategy for those that understand the information of how it works and are willing to approve the prices and constraints associated with this financial investment

Select the "riches" alternative as opposed to the "estate" alternative. Most companies have 2 different kinds of Whole Life strategies. Choose the one with higher cash worths previously on. Over the course of numerous years, you add a significant quantity of cash to the policy to construct up the cash money value.

You're essentially lending cash to yourself, and you repay the financing over time, typically with passion. As you pay back the funding, the money value of the policy is renewed, permitting you to obtain against it again in the future. Upon fatality, the survivor benefit is minimized by any type of impressive financings, but any staying death advantage is paid out tax-free to the recipients.

How do I leverage Financial Independence Through Infinite Banking to grow my wealth?

Time Horizon Danger: If the insurance holder determines to terminate the plan early, the money abandonment worths might be substantially reduced than later years of the policy. It is advisable that when discovering this strategy that a person has a mid to long term time horizon. Tax: The insurance holder may incur tax consequences on the fundings, returns, and survivor benefit repayments got from the plan.

Intricacy: Limitless financial can be intricate, and it is vital to recognize the information of the plan and the cash money accumulation component before making any kind of financial investment decisions. Infinite Banking in Canada is a legitimate economic technique, not a fraud. Infinite Financial is a concept that was established by Nelson Nash in the USA, and it has actually considering that been adjusted and applied by monetary experts in Canada and various other nations.

Plan fundings or withdrawals that do not go beyond the adjusted expense basis of the plan are taken into consideration to be tax-free. If policy loans or withdrawals surpass the modified cost basis, the excess amount might be subject to tax obligations. It is crucial to keep in mind that the tax benefits of Infinite Banking might undergo change based upon modifications to tax obligation regulations and policies in Canada.

The dangers of Infinite Banking include the possibility for plan loans to reduce the death advantage of the policy and the opportunity that the policy may not carry out as expected. Infinite Financial might not be the very best technique for everyone. It is essential to thoroughly think about the costs and potential returns of joining an Infinite Banking program, along with to thoroughly study and recognize the connected threats.

How does Policy Loans create financial independence?

Infinite Banking is different from conventional financial because it allows the policyholder to be their own resource of funding, as opposed to depending on standard banks or loan providers. The policyholder can access the cash value of the plan and utilize it to finance acquisitions or investments, without needing to go with a typical lending institution.

When the majority of individuals need a lending, they apply for a line of credit score with a conventional bank and pay that finance back, over time, with interest. For doctors and other high-income income earners, this is possible to do with unlimited banking.

Right here's an economic consultant's review of boundless banking and all the pros and cons included. Boundless banking is an individual banking strategy created by R. Nelson Nash. In his book Becoming Your Own Banker, Nash clarifies how you can make use of a long-term life insurance coverage policy that builds money value and pays dividends therefore freeing yourself from needing to obtain money from lenders and pay back high-interest finances.

What are the benefits of using Financial Independence Through Infinite Banking for personal financing?

And while not everyone gets on board with the concept, it has actually tested numerous hundreds of individuals to reconsider how they financial institution and just how they take finances. Between 2000 and 2008, Nash launched six versions of the book. To now, financial consultants consider, method, and question the concept of infinite financial.

The limitless financial principle (or IBC) is a bit more complex than that. The basis of the limitless financial principle starts with long-term life insurance. Infinite banking is not feasible with a term life insurance plan; you need to have a permanent cash money worth life insurance coverage plan. For the idea to work, you'll need among the following: a whole life insurance coverage policy a global life insurance coverage policy a variable global life insurance policy plan an indexed global life insurance policy If you pay even more than the required monthly costs with permanent life insurance policy, the excess contributions build up cash value in a money account. Infinite Banking retirement strategy.

Yet with a dividend-paying life insurance policy plan, you can grow your cash money worth also quicker. Something that makes entire life insurance policy distinct is gaining a lot more money via rewards. Mean you have a long-term life insurance coverage policy with a common insurer. Because situation, you will be qualified to receive part of the company's revenues much like exactly how investors in the company obtain rewards.

{kind=link}

Latest Posts

Unlocking Wealth: Can You Use Life Insurance As A Bank?

Life Insurance Be Your Own Bank

Can You Be Your Own Bank